How to Get the Best Deal

on Atlanta Home Mortgage Loans

Here's

my advice in a nutshell. Shop on the Internet and then use a local lender you

can trust who can also match those rates.

Don't trust any advertised rates. There are always details they never

mention. They will say anything to make their phones ring. Once

they have you on the phone, they'll suck you in and sell you a product you

could have gotten anywhere else.

So, who can you trust?

I've been a real

estate agent for 16 years and have met a lot of loan officers. Many

are very good at what they do. Others, I wouldn't trust for a minute.

My five best recommendations are as follows because all four:

Offer very competitive rates. They don't mess

around

Get the job done. If they say you are approved,

you are approved

Will get you the HUD-1 statement 48 hours before

closing

Will attend the closing to make sure nothing goes

wrong

Will give you a Good Faith Estimate that you can

trust

Are really motivated. If they screw up, they

are off my list and no more referrals

Let all five give you a quote. It's a crazy, competitive market with

changes happening daily. If shopping, make sure you get quotes at the

same time and day.

A

federal

law was passed in 2008 that required the credit agencies to supply you

with a free credit report at least once per year.

As you'll see on the federal website, there is an

official site where you go to get your free credit report.

www.annualcreditreport.com

It's

kind of a hassle going through and getting your report at all three credit

agencies, Experian, Equifax, and Trans Union. They also don't give you

your credit score. They give you information about all of your credit

accounts but they make you pay to get their credit score. It's about

$6-$10 each. The problem is that the scores they give you aren't the

same scale that the lenders use and talk about. These scores they give

you are from 500 to 990. So it's kind of a waste of money.

Usually

it's just a lot easier having a lender do a free credit report for you.

Just have one lender run your report and supply you with a copy. The

lender will also be able to translate the data and tell you what it all

means. Lenders pull credit reports all the time and usually don't charge

you upfront.

2.

Check out rates at The Mortgage

Professor. This will give you a

good foundation to make comparisons with. Make sure you compare apples

with apples. Make sure lock periods, credit score assumptions and impounds are

all comparable. Here is their

daily mortgage price page

3. Call a

few local

lenders who were recommended to you by someone you trust. A good loan

advisor is such a great value. They can make sense out of all the various

programs and advise you on what's best for you. When they see that you

have all of your financial documents in order and you have been shopping around,

they will most likely give you their most competitive rates from the get

go.

4. Make sure you

compare "apples with apples". The cost of the loan is not just the

interest rate. It's the combination of interest rate and the

associated lender fees. When comparing lenders, just

compare the closing costs that are lender related. Don't go messing

around other closing costs that the lender has no control over. We'll

deal with those separately and make sure we get the best deals for each

service.

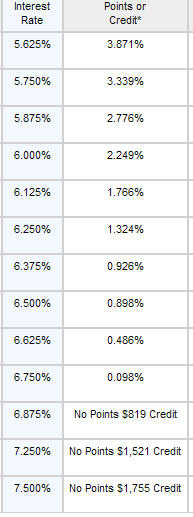

Pick an interest rate and get the

total loan costs associated with that particular rate. The higher

the rate, the less the lender fees will be. Below is an example

how interest rates will change with the number of points you pay.

Starting on January 1, 2010, All

lenders will be using the same Good Faith Estimate (GSE) forms.

This hopefully will make it easier to compare proposals. There are

also new regulations which will require lenders to honor their estimated

costs up to a certain limit. This is supposed to keep the lenders

from supplying customers with unrealistic "estimates".

I don't get anything by

recommending the above loan officers except the knowledge that I can trust them to give my

clients great service.

If you go with a random lender, you end up just

being another number. If they mess up your loan, you are just one of many

other loans they have in process. With my recommendations, if you mention

my name, they know that if they don't perform, it just isn't your loan

they're losing,

but all of the future referrals I might send their way.

I've

seen many clients get suckered in with all of the claims of "no closing

costs" or some really low ball rates. I will admit, I'm always on the

look out for the best deals and often get drawn in by some amazing offer. But when I finally get someone

on the phone or get a good faith estimate statement, it always seems like the

seductive rates always seem to slip away. All of those things are just

hooks to get you in the door. Then when you finally see all of the

details, it's usually not any better than what a local lender with full service

can provide.

If

you get a really low rate, make sure your "lock in" is in writing. Some

shady loan officer might be speculating that by the time of your closing the

rates will have gone down and he'll be able to honor those low rates. If

the rates go up before closing, the lender will find some sort of technical

detail to deny you the loan, not a nice thing to have happen when you have

everything all set up for the big move. If the lender is out of town

you'll never get them on the telephone. They won't care. You are

just one of many loans.

Don't

get fooled about someone offering no closing costs. There is no such thing

as a free lunch. Banks have employees that must get paid. There are

definitely costs involved in originating a new loan. They either can be

itemized so you know exactly what you are being charged for or they can

be hidden by being incorporated into the loan rate or points. You might get "no

closing costs" but you'll be paying a higher interest rate or more points.

If

you do happen to find a lender who really can offer some really low rates with

really low closing costs, be prepared for really little service. You'll

place a call and will get a different person every time who really doesn't care

if your loan closes on time or not. They get paid by the hour, not by the

sale. That's if you're lucky enough to get someone at all. Most

likely you'll get a computerized answering system that will walk you through a

series of confusing choices and leave you swearing at the phone. You get

what you pay for.

Everyone's

risk tolerance is different. If I were just refinancing my mortgage to get

a better rate I might take a chance with an unknown lender with little

service. If it didn't close it wouldn't mess up my life.

But

if I were selling my home and moving to another home and had things packed and

movers coming at a specific time, I sure wouldn't want to take a chance on my

loan not closing. No amount of savings would cover the stress and the

hassle of a delayed closing.

Whatever

lender you choose, it really helps to get the loan process going early on in

your home search. That way, when you find a great home, you'll be in a

powerful negotiating position by being pre-approved.

So

get pre-approved and then call us when you're ready to go find the home of your

dreams.

Sincerely,

Tim

Maitski

Atlanta Communities Real Estate Brokerage

cell 404-216-0472

Our market area is in the

north metro Atlanta area.

We service Cobb County,

north Fulton County, Dekalb

County, Forsyth County and

Gwinnett County. We

are very familiar with Sandy

Springs, Dunwoody, Marietta,

Roswell, Alpharetta,

Buckhead, and Midtown.

We have sold homes inside

the perimeter and outside

the perimeter. We

can't know everything so for

clients who want to look for

property in Peachtree City,

Newnan, Stone Mountain,

Douglasville, Macon and

areas further out we will

gladly recommend a good

agent who specializes in

those areas.

We help buyers negotiate

with builders for

residential new construction

houses. New houses in

Atlanta are hot right now.

We can represent you in the

purchase of your new house

built by any of the

following builders: Torrey

Homes, MDC Homes, Centex

Homes, Pulte Homes, Morrison

Homes, Ryland Homes, John

Wieland Homes, Winmark

Homes, Meridian Homes, John

Willis Homes, Benchmark

Homes and many more home

builders.

We can help clients find

short term apartments for

rent but normally we don't

work with clients who are

just looking for rentals.

We do help clients find

Atlanta condos. We can

also help you purchase HUD

homes in Atlanta. We

are an authorized agent with

them and have the HUD key to

get into HUD homes. We

have access to foreclosure

homes that banks want to

sell.

We love showing executive

homes and luxury homes. We

always like to know how

people find our site.

Send us an email and tell us

which search term you used.

Some terms that we might be

found by are realty Atlanta,

Ga homes, Atlanta realty,

condos Atlanta, Atlanta

realestate, Atlanta

property, houses Atlanta,

Atlanta realtors, Ga houses,

or realtors Atlanta.

Maybe you found us by typing

in Atlanta MLS listings, or

Atlanta MLS search, or MLS

Atlanta GA. Hopefully we

don't come up under nursing

homes or funeral homes.

It is always amazing to me

how the Internet can allow

total strangers to find each

other and build new business

relationships. It

truly is becoming a small,

interconnected world.